The Role of Unit Economics in P2P Lending Business

In the vast world of finance, the lending business remains one of the most complex but important parts. Every transaction, every loan issued, and even every promo code extended reflects a complex dance of numbers and strategy. At the center of this dance is a concept that stands as the backbone of understanding profitability and sustainability: unit economics.

Drawing from our experience, we share this article to give you a more in-depth understanding of how unit economics works. We'll journey through the intricate details of the lending sector, deciphering how unit economics provides pivotal insights that drive success in this industry.

What is Unit Economics?

Unit economics offers a lens through which a company's business model can be scrutinized. At its core, unit economics zeroes in on ensuring that the production and sale of every individual unit of a product is profitable, emphasizing that revenues consistently surpass costs.

Distinct from traditional financial metrics, unit economics delves deeper, highlighting and refining each step involved in the creation of a product or service. This approach offers businesses a clearer pathway to optimize each phase of production and enhance profitability.

Understanding the 'unit economics meaning' is vital for businesses, as it sheds light on the profitability at the most granular level, guiding companies to make informed decisions about pricing, production, and overall business strategy for sustainable growth.

Decoding Unit Economics in the Lending Business

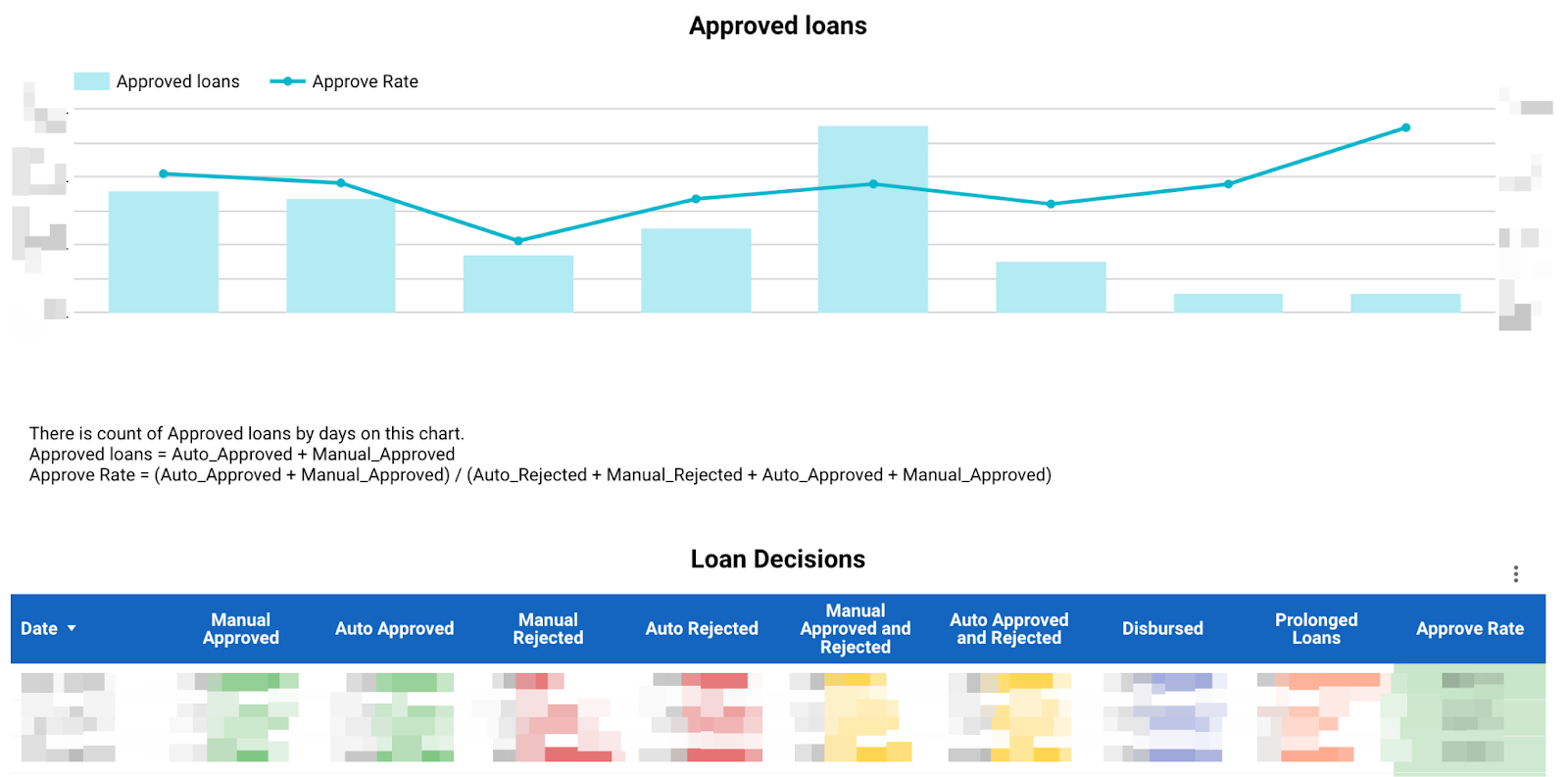

Upon an initial overview, lending might seem elementary: lend money and accrue interest. However, diving deeper reveals an intricate science. Our partners (loan originators) often work with more than 200 real-time reports, each digitized and nuanced. Each report is not just a mere number but represents comprehensive analytics, a defined process, and dedicated personnel.

Here is a sample report. Any sensitive or commercially significant details have been concealed, solely for illustrative purposes.

These individuals manage and optimize these figures to ensure maximum benefit to the entire organization. For instance, we have a dedicated Product Manager who solely focuses on registration. Her primary goal is to ensure that out of 100 clients who start the registration process, we grant loans to all 100. Therefore, they scrutinize and analyze each step of the registration, noting how many clients drop off and how many seconds it takes to fill out each field. If we're talking about risk managers, on the other hand, aim to extend loans to the maximum number of clients possible.

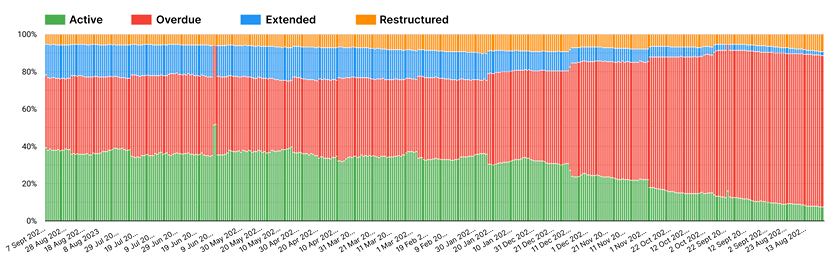

1. Active portfolio

A foundational principle in the lending business is the size of the active portfolio. This portfolio is where interest is accrued. Thus, the larger your active loan portfolio, the greater your earnings. It's essential to note that the active portfolio is merely a segment of a company's total loan portfolio, which also includes categories like overdue, restructured, and extended portfolios. While all these portfolios are revenue-generating, the primary focus remains on the size of the active portfolio.

To visualize the lending business, imagine a bathtub with water (money) constantly flowing in and out. The objective is to keep the bathtub optimally filled – neither overflowing nor running dry. The water diminishes when there are arrears and refills with every loan issued.

Here is an example of a Ukrainian portfolio:

2. Average Check

Central to this mechanism is the “average check” size, which revolves around credit applications – the heart of the lending business. With an investment of X dollars in marketing, a potential client is acquired. Only when this user applies to do they transition from a prospect to a customer.

Monitoring the enrollment funnel is vital. It's crucial to understand the drop-off at every stage, aiming for a 100% completion rate. Specialized teams within our partner diligently oversee each funnel stage, striving for its perfection.

3. Approval rate

Another key metric is the approval rate of loan applications. Risk managers oversee this process, evaluating each client's credibility and determining loan eligibility. Our conversation in Lonvest Blog with Timur Bugayevsky, Head of Data Since Lab shed light on the intricacies of managing risks in lending.

Though the issued credit is a crucial metric in unit economics, it's merely the surface. Major decisions and costs come into play well before a loan is sanctioned.

Breaking down the customer journey into units reveals:

-

Cost per application: Marketing expenditure for each submitted application.

-

Registration conversion rate: Percentage of customers completing registration.

-

Approval rate: Percentage of approved loan applications.

-

Scoring Cost: Expense for scoring a single application.

-

Average check: Mean loan amount disbursed.

-

Loan frequency: Number of loans disbursed daily/monthly.

-

Loan portfolio volume: Total amount disbursed to clients and its classifications – active, restructured, overdue, and extended.

-

Default rate: Percentage of loans defaulting at various intervals.

-

Recovery Ratio: Percentage of repayments to overall debt in a given period.

These indicators are just a snapshot. Each can be broken down further into more detailed metrics, with processes for each being increasingly digitalized.

In essence, the lending business operates like an orchestra. Seamless coordination among all participants ensures the collective's success. The overarching aim for every CEO in the lending domain is to fine-tune each business process for peak efficiency. Every indicator, every request, and every detail matters – nothing should slip through the cracks.

Influences on Unit Economics in Lending Business

Delving into the intricacies of the lending business reveals a plethora of factors that can significantly sway its financial outcomes. Factors as seemingly mundane as the time of day, the position of a date within a month, or even the number of holidays in a given month can play a crucial role. Beyond these immediate influences, broader economic indicators — like the country's GDP, unemployment rates, and the overall economic climate — also hold considerable weight.

Incorporating unit economics in business is pivotal in this context. This approach focuses on understanding the profitability and cost-effectiveness of each transaction or customer interaction within the lending business. It allows for a more nuanced and granular analysis of how individual elements contribute to or detract from the overall financial health of the organization.

However, merely identifying these influencing factors isn't enough. The true value lies in leveraging this knowledge for proactive management.

Effective portfolio management within one month

For instance, if we anticipate a month with more holidays ahead, we can strategically adjust our turnover plans to ensure consistent cash flow, thus catering efficiently to our customers' demands. Similarly, if projections suggest a potential 1% decrease in funds for the upcoming month, it's vital to be prepared. This foresight ensures that the business can handle an unexpected surge in loan requests without any interruptions.

Integrating Unit Economics into Risk Management

At its core, risk in the lending business seems binary: either a client repays the loan (1) or they don't (0). However, when we delve deeper beyond this binary perspective, we uncover a nuanced landscape of data points:

-

When will the repayment occur? (Promptly? Late? If late, by how many days?)

-

How much interest will the client pay?

-

What resources will be expended to ensure repayment?

By scrutinizing each step in the lending process, we can fine-tune risk management strategies. Consider, for example, the average rate of a loan issued.

How sales and promotions work in the landing business

An intriguing observation is that when customers are offered more promo codes, they tend to request a larger loan amount, and paradoxically, are more likely to repay it. One might assume the contrary – that repaying a larger amount would be more challenging. But the rationale is straightforward: every conscientious borrower gauges how much they can comfortably repay in the near term (e.g., within 10-30 days). Thus, if a borrower knows they can manage a repayment of 100 EUR in 10 days, they might opt for a loan of 100 EUR with a 10 EUR commission, given a certain promo rate. But, with a more generous promo code (resulting in a lower interest), they might apply for 115 EUR and pay just 5 EUR commission.

Conversely, clients who have no intention of repaying are well aware of their plan even before applying. They might borrow at any interest rate, no matter how exorbitant. To them, the rate is irrelevant. This relationship between the size of the interest rate and risk highlights the intricate dynamics of lending.

Integrating Unit Economics with Strategy to Maximize Customer LTV

The short term lending caters usually to those who might not be served by traditional banks. Consequently, the Lifetime Value (LTV) of customers in this sector presents unique challenges. Some customers progressively improve their financial standing, borrowing less frequently and eventually becoming eligible for bank loans. Others might face declining financial circumstances, and lending institutions, aiming to avoid pushing clients further into debt, might cease providing them with loans.

This delicate balancing act entails assisting clients while distinguishing responsible borrowers from the less responsible ones and ensuring we don't overburden them financially. A common grievance among customers is dissatisfaction with the loan amount or the average check provided. However, setting this average check is not arbitrary; it's designed to align with an amount the borrower can realistically repay. Similarly, when determining interest rates, the objective is twofold: ensuring loan repayment while fostering a perception of fairness in the customer’s eyes. In essence, by strategically adjusting the average check and interest rates, lenders aim to guide and educate their clientele, warding off potential debt pitfalls.

Incorporating unit economics of business into this equation is critical. By comprehensively understanding factors like the cost of customer acquisition, funnel conversion rates, the expenses linked with client authentication and scoring, and the average loan tenure, lenders can astutely decide which loans to grant, to whom, and at what interest rate. Such a nuanced approach ensures the sustained operation of the lending mechanism.

The pursuit of excellence

The dance of numbers in the lending business is not just about issuing loans and expecting returns. It is about understanding, strategizing, and optimizing each tiny component that impacts the broader picture. Unit economics serves as a beacon, guiding businesses through the intricate pathways of the lending landscape. By embracing and implementing the principles of unit economics, lending businesses can ensure that they not only survive but thrive in a challenging financial environment. As the world of lending continues to evolve, those equipped with the profound insights provided by unit economics will undoubtedly lead the way.

If you're considering the opportunity to invest in loans, then Lonevest offers the perfect gateway to begin this venture.

Lovinčićeva street, 3, Zagreb, Croatia